Highlights from "Option Volume Imbalance as a Predictor for Equity Returns"

Highlights for the paper Option Volume Imbalance as a Predictor…

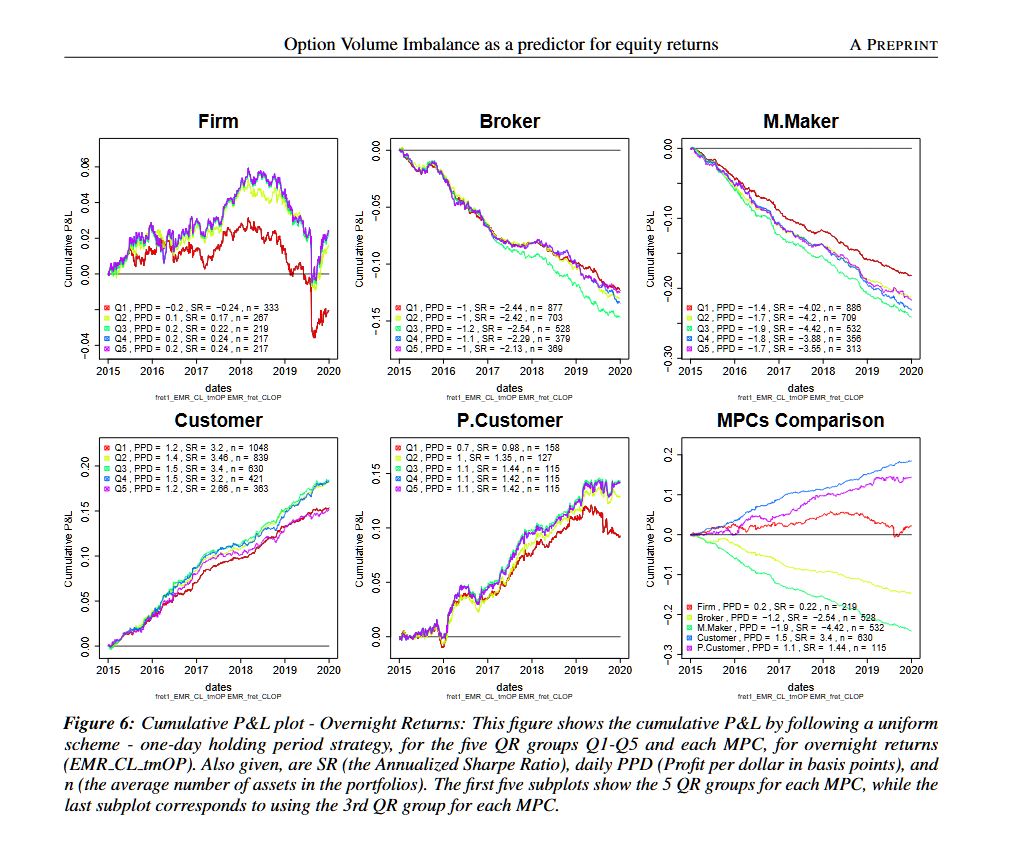

Insights

-

…deep out-of-the-money options had the highest predictive power, as well as data that came from customers who traded using full-service brokerage house (Pan and Poteshman, 2006)

-

…option volume flow metric was defined by [ Hu, 2014 ], who used delta-adjusted volumes and showed its significant predictive power for stock returns.

-

… found that the predictability of future returns is stronger for assets with a higher ratio of informed traders, low analyst coverage, large bid-ask spreads, small market capitalization, and low institutional ownership.

-

cross MPCs, higher Gamma options/higher Gamma buckets (corresponding to ATM options) tend to perform better

-

Results are not as clear with moneyness buckets, with no consistent pattern followed by the buckets, except that the 1st bucket is outperformed by the rest, hinting that deep OTM options have the lowest informational content

-

no consistent pattern can be observed across MPCs for the different maturity buckets, indicating that maturity has no effect on predictability

- We can clearly observe that put options play a more important role in predicting future returns compared to call options…

- Across all MPCs, the first bucket for Delta (consisting mostly of ITM put options) outperforms the other buckets…

- Customers, the 1st bucket significantly outperforms the other buckets

- For all of Brokers, Market Makers, and Customers, higher implied volatility results in higher predictability

- Similarly to the volume weighted betting scheme, we consider a strategy based on the product’s volume, multiplied by the implied volatility of the asset. We set the IV-Volume Weighting Scheme

- For Vega, no consistent pattern can be observed across MPCs. Thus, while implied volatility plays a big role in determining the informational content of an option’s volume, the sensitivity of options to implied volatility does not

Conclusions

-

for Customers most of the predictability comes from the selling activity

-

option characteristics that seem to consistently induce higher performance include negative values for Rho, and negative values for Delta (i.e put options)

-

the OVI from high implied volatility contracts is significantly more informative than option contracts with low implied volatility